You have submitted your tax return and now you know your self assessment tax bill - what you owe the taxman!

How then do you go about paying HMRC?

When should you make payment?

That’s where self assessment payment on account comes in. It applies to UK tax payers where less than 80% of your income has tax deducted at source. This means under 80% of the tax is deducted from your income before you receive it, an example being where an employer pays an employee under the Pay As You Earn (PAYE) system.

By reading this blog you'll find out how the payment on account system works, why you should set money aside for settling your tax bill, and the importance of your tax return and planning to this process. Most importantly, you'll then likely understand how HMRC have calculated the bill that's presented on the final page of your tax return.

In this post we cover:

Payment on account applies, potentially, to people in the UK self assessment system. It’s the system for settling tax owed from the tax return. Payment is spread over two installments during the year and is calculated based on the previous year's tax bill.

It works on the basis whereby you make an advance tax payment in part. This is designed to prevent you from being indebted to HMRC. In the event that the tax liability is greater than the previous year, a further balancing payment may also be required.

This may all sound simple but there are many aspects and rules. That's why we’ve put this post together, to give you a thorough understanding of this process because it can get quite complicated.

Of note, in no way should you substitute this information for taking sound professional advice. Gaining an understanding will provide you with insight into the complex nature of the self assessment process and the need to:

The first payment date is midnight on 31 January. That's prior to the end of the tax year in question. It's calculated by looking at your previous year’s tax bill. The deadline for the second installment is midnight on 31 July, after the end of the tax year in question.

This spreads your payments out over the course of the year. It helps the Exchequer too. They receive in effect a forward payment by the summer.

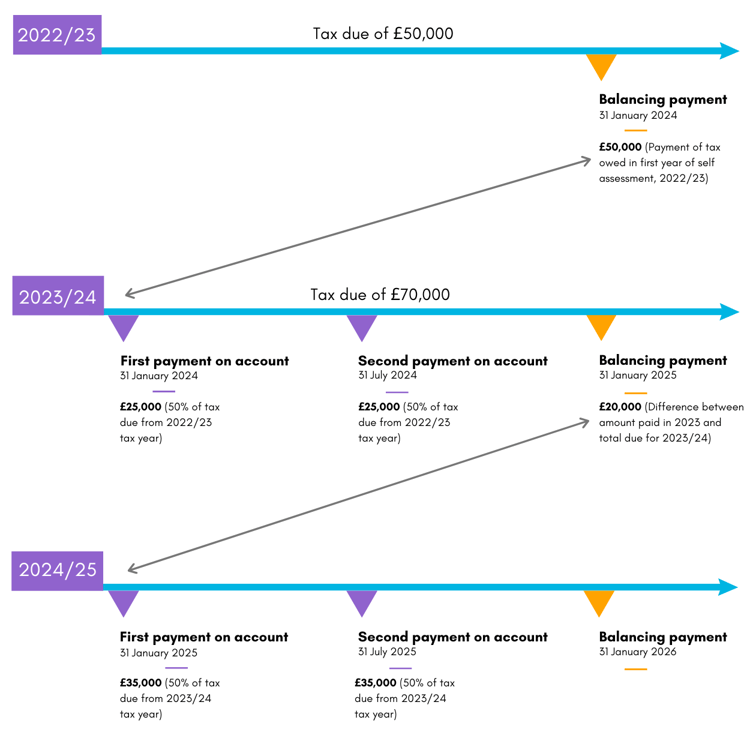

Each of your installments will usually be 50% of your previous tax bill. Consider the following simple, hypothetical example. You owe £50,000 in tax for the first time under self assessment for the 2022/23 tax year. This is due for payment on 31 January 2024. You would have to make a first payment on account of £25,000 by 31 January 2024. Then another £25,000 by 31 July 2024.

Simple right? Not so unfortunately. Read on because you may need to factor in a “balancing payment”. That may then impact on your payment plan.

This is where confusion can arise.

Check the diagram above to help you with this. You’ve paid a total of £50,000 by 31 July 2024 based on your 2022/23 tax bill. However, your total tax owed for the 2023/24 tax year comes in at £70,000 based on your 2022/23 tax return.

That means you have an outstanding balance of £20,000 (£70,000 owed minus the £50,000 paid by 31 July). This is called the balancing payment. It has to be settled by 31 January 2025. Your 2024/25 payment plan would work as follows.

Total tax to pay on 31 January 2025 of £55,000 consisting of:

You won’t have to make two payments in the year if:

It can become problematic if you earn a lot of income one year and this then drops significantly the next. You may foresee a cash shortage if you know for certain that your tax bill will be lower than the previous year. You'll need to request that HMRC reduce payments on account.

Be warned, don't reduce your payments on account by too much in your tax account. HMRC will charge you interest and penalties for underpaying. Alternatively, HMRC can refund you if your payments are greater than your total tax bill.

This excludes sums you may owe for capital gains or student loans. Instead, these items are covered in your balancing payment.

You can access what you owe the tax man through HMRC online services. It provides you with the payments you need to make in January and July. It also gives you access to historical payments on account.

This all highlights the need to be putting money aside regularly. You'll then be able to fulfill your tax payments at the beginning and mid point of every calendar year. Find an advisor to help you put in place a tax payment plan. That way you can manage your personal finances effectively.

You can settle what is owed using the following payment methods:

Consider carefully that it takes 3 working days to process a payment via bacs, direct debit (if you’ve already set it up) and cheque (upon receipt). Be sure to factor that in around the deadline. If you haven’t set up a direct debit arrangement then remember that the first payment will take 5 working days.

If the payments on account deadline falls over a weekend or bank holiday, you need to make sure your payment reaches HMRC on the last working day prior to the weekend in question.

Being tax efficient is a process that starts with your tax return. We've written a piece about how to be better prepared for your online tax return. Here's a summary of the benefits of submitting it before the deadline:

1. Refunds

Filing your tax return early (before the 31 January deadline) will mean you should receive any tax refund you may be due, soon after submission. In instances where you think you have overpaid tax, be sure to get your return in as promptly and early as possible. That way you can obtain your refund sooner.

2. Payment and cash planning

Filing your tax return results in a tax liability calculation. This presents you with the total tax bill you owe to HMRC. Doing so earlier means you can plan. That way you can give yourself more time to set money aside for payment. This allows you to better manage your cash flow and finances.

Also, if your tax liability comes in under £3,000 and you submit your tax return in December, then you have the option of your tax liability being paid through your tax code. It will be deducted from your wages or pension at whatever interval arrangement you have set up (weekly or monthly).

3. Tax planning - how to reduce payments on account

Your income might vary markedly from one year to the next. Whether a significant increase due to a dividend payment or, a steep decline as a result of trading losses, early submission provides more time for tax planning.

That means you (and/or your advisor) have sufficient time to assess your circumstances. You can then assess where you might be paying more tax than you legally should be. Savings might then be achievable.

Rushing your tax return in just before the deadline is risky. It's more likely to lead to errors. There's likely to be less time for checking the accuracy of what is stated compared to your income streams. You’ll need time to assemble financial documents and bank statements to fill in your return properly. If HMRC uncover errors you’ll be subject to penalties.

What if you have a query and need help from HMRC? You’ll have to phone their helpline. That's a notoriously time consuming process. It’s even worse during tax return season in January. Their lines are bombarded with these kinds of calls. Avoid it if you can! It could impact on your submission.

5. Your tax advisor/accountant

Your accountant will likely deal with a lot of tax returns on behalf of their clients. Especially in January! If you provide your information close to the deadline then you could end up rushing when collating information and missing out key items from the data you supply. The risk then is a late filing. A situation your accountant might not be able to avoid.

So, if you're required to fill out a self assessment tax return then you'd do well to follow this plan. That way potential savings can be achieved and late payment penalties avoided:

As the saying goes, “fail to plan, plan to fail”.

This post was created on 29/07/2016 and updated on 15/06/2023.

This post was created on 29/07/2016 and updated on 15/06/2023.

Please be aware that information provided by this blog is subject to regular legal and regulatory change. We recommend that you do not take any information held within our website or guides (eBooks) as a definitive guide to the law on the relevant matter being discussed. We suggest your course of action should be to seek legal or professional advice where necessary rather than relying on the content supplied by the author(s) of this blog.

leave a comment -