Treasury and IRS Issue Guidance on the Qualified Alternative Fuel Vehicle Refueling Property Credit

As reported via IR-2024-16 on 1/19/2024

The Internal Revenue Service and the Department of the Treasury today issued Notice 2024-20 to provide guidance on eligible census tracts for the qualified alternative fuel vehicle refueling property credit (the tax credit applicable to the installation of EV chargers) and to announce the intent to propose regulations for the credit.

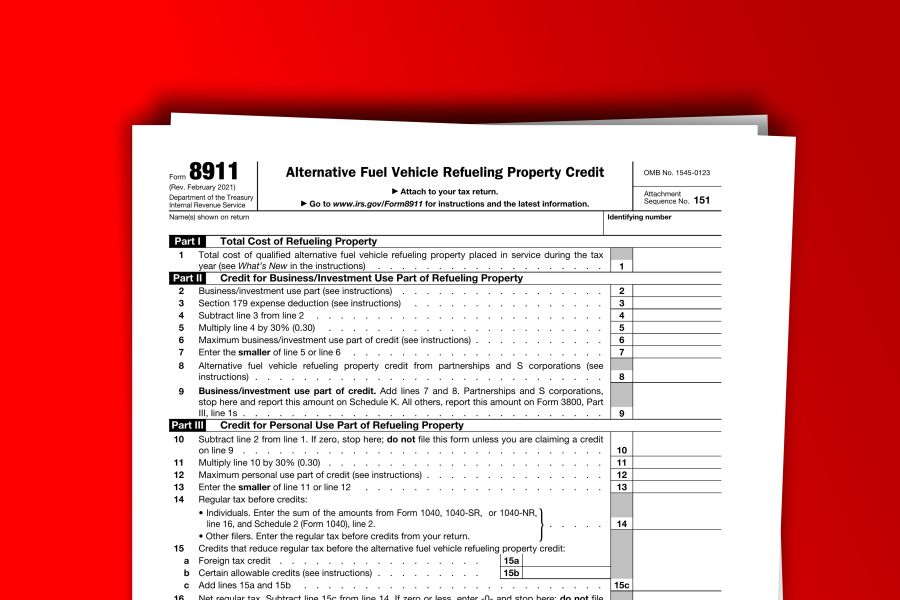

The Inflation Reduction Act amended the credit for qualified alternative fuel vehicle refueling property. The changes apply to qualified alternative fuel vehicle refueling property placed in service after December 31, 2022 and before January 1, 2033.

Business vs Non-Business Property

Property Not Subject to Depreciation

The credit amount for property not subject to depreciation is 30% of the cost of the qualified property placed in service during the tax year. The credit is limited to $1,000 for non-depreciable property.

Property Subject to Depreciation

The credit amount for depreciable property is 6% of the cost of the qualified property placed in service during the tax year but may be increased to 30% of the cost of the qualified property if the prevailing wage and apprenticeship requirements are met. The credit is limited to $100,000 for depreciable property.

Geographic Location of Property

Property must be placed in service in an eligible census tract to qualify for the credit. An eligible census tract is any population census tract that is a low-income community or any population census tract that is not an urban area. See Appendix A and Appendix B for eligible census tracts.

The primary purpose of the notice is to provide taxpayers with a list of eligible census tracts in advance of the 2023 filing season and to explain how taxpayers can identify the 11-digit census tract identifier for the location where the property is placed in service. The IRS intends to propose regulations including this information in the future, but taxpayers may rely on the notice until proposed regulations are published.

Mapping Tools

Taxpayers can determine the 11-digit census tract GEOID of a location under the 2020 census tract boundaries as follows:

Using Address Location

https://geocoding.geo.census.gov/geocoder/geographies/address?form

Using Latitude/Longitude Point

https://geocoding.geo.census.gov/geocoder/geographies/coordinates?form

Other Information Provided

This notice also provides background and definitions, describes relevant census concepts, provides definitions for low-income communities and non-urban census tracts, and explains which delineation of census tract boundaries is applicable for each type of census tract determination. Further, the notice describes how updating of low-income community census tract determinations are considered for credit eligibility.

Resources

- IRS FAQs related to the alternative fuel vehicle refueling property credit.

- More information about the alternative fuel vehicle refueling property credit.

- Information about the Inflation Reduction Act of 2022.

(This is Blog Post #1517)