Payroll

How Accounting and Tax Pros Can Help Clients Strategize on Social Security

The ideal age to claim Social Security benefits varies for everyone based on their unique financial situation, health, life expectancy, and overall retirement plan.

Oct. 17, 2023

By Bhairavi Parikh, CPA.

Social Security is a program designed to offer retirement benefits and disability income to eligible individuals, as well as their spouses, children, and survivors.

In 2023, an average of almost 67 million Americans per month will receive a Social Security benefit totaling about $1.4 trillion in benefits paid. Out of 67 million, 52 million are retired, 8.7 million are disabled, and 5.8 million are survivors. Sounds like a lot of our population, but at the same time, eligible people will miss out on taking the full Social Security benefit simply because they were unaware of the rules and strategies around it.

That’s where you come in. As your client’s trusted advisor, your role starts early on when you’re working with individual and business clients—often while they are still in their earning period and continuing until full retirement age … but the rules and benefits can be really confusing. Here’s a summary of the rules, benefits, and strategies around Social Security benefits throughout a person’s lifespan.

Earning years and eligibility

To qualify for Social Security retirement benefits, individuals must have reached the age of 62 and contributed to the system for at least 10 years, which is equivalent to 40 credits. Benefits are based on the highest 35 years of earnings. Workers can earn up to four credits each year. For every $1,640 earned in 2023, one credit will be granted up to $6,560.

Pro tip: Check your Social Security credit here.

Here’s what you need to know:

- If the individual works for an employer, the Social Security tax is withheld from the paycheck and gets reported by their employer through payroll taxes. It is important to note that if the individual is receiving a W-2, the individual and their employer each share the tax burden of 6.2%. Here, the employer matches the amount toward the person’s Social Security.

- If the individual is self-employed, they will be responsible for contributing both the employee and employer portion, and also to report it along with self-employment taxes.

- When the individual retires or becomes disabled, the government uses the individual’s history of Social Security wages and tax credits to calculate the benefit payments they will receive.

Unlike contributions to traditional retirement accounts such as a 401(k) or IRA, the funds you pay into Social Security are not tax-exempt or tax-deductible on your annual tax return.

Claiming years if you’re due to retire

The ideal age to claim Social Security benefits varies for everyone based on their unique financial situation, health, life expectancy, and overall retirement plan. There’s no one-size-fits-all answer. However, here are some considerations to help determine the optimal age to claim Social Security benefits:

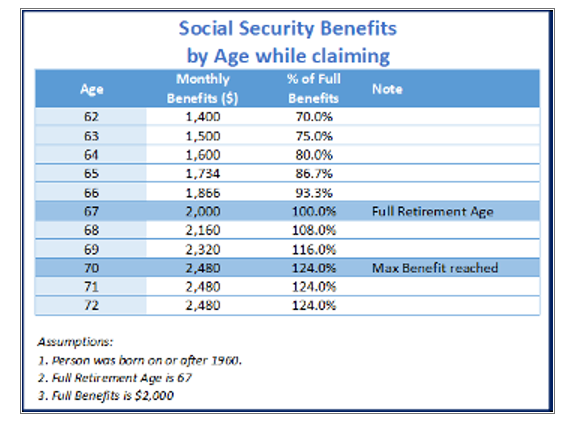

- Full Retirement Age: The Full Retirement Age (FRA) is the age at which you can receive your full Social Security benefit amount. FRA varies based on the year you were born, but it’s typically between ages 65-67. Claiming at FRA ensures you receive 100% of your benefit.

- Early retirement: You can choose to start receiving reduced benefits as early as age 62. However, your monthly benefit will be permanently reduced compared to what you would receive at FRA. Cost-of-living benefit adjustments begin at age 62, regardless of when you decide to claim your benefits.

- Delayed retirement: You can delay claiming benefits after reaching FRA, up to age 70. For each year you delay, your benefit increases by a certain percentage, resulting in a higher monthly benefit when you do claim.

Research suggests, on average, that Social Security will likely make up only about 30% or less of a person’s pre-retirement income. The easiest advice you can give is to consider health and working capabilities before deciding to take retirement benefits. If someone is in healthy condition and can still work, they should delay claiming the benefits.

Can you still work while claiming Social Security benefits?

The answer is yes. However, if you are younger than full retirement age and make more than the yearly earnings limit, your benefit will be reduced. However, if you start with the month you reach full retirement age, you will not reduce your benefits no matter how much you earn.

Note that up to 85% of your Social Security benefits can be taxable. Limit your other business income by using some of these tax strategies:

Individual:

- If your reported income is between $25,000 and $34,000, you may pay taxes on up to 50% of your benefits.

- If your reported income is more than $34,000, you may pay taxes on up to 85% of your benefits.

Married filing jointly:

- If your reported income is between $32,000 and $44,000, you may pay taxes on up to 50% of your benefits.

- If your reported income is more than $44,000, you may pay taxes on up to 85% of your benefits.

Spouse and dependent benefits

The individual’s spouse may be eligible for a benefit based on their earnings. One of the requirements is that the spouse must be at least age 62 or have a qualifying child in their care. If your benefit amount as a spouse is higher than your own retirement benefit, you will get a combination of the two benefits that equals the higher amount.

Claiming years due to disability

In addition to retirees, individuals unable to work due to disability—and surviving spouses and children—may also qualify for benefits, provided they meet specific criteria. Social Security benefits play a critical role in providing financial support and security to individuals facing disabilities. The Social Security Administration (SSA) offers various programs designed to aid disabled individuals and their families during challenging times.

Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI) are the two primary federal programs that provide financial assistance to individuals with disabilities. These programs aim to offer a safety net, and ensure a basic standard of living for those who are unable to work due to a severe and long-term disability.

- Social Security Disability Insurance: SSDI provides benefits to disabled individuals based on their work history and earnings. To qualify, individuals must have a qualifying disability and earned enough work credits through their employment history. The amount of benefits is based on the individual’s average lifetime earnings before becoming disabled.

- Supplemental Security Income: SSI is a need-based program designed for disabled individuals with limited income and resources. Eligibility is not based on work history, but rather on financial need. SSI provides a basic monthly payment to help with living expenses. It may also grant access to Medicaid in many states.

To be eligible for Social Security disability benefits, individuals must meet specific criteria established by the SSA. Advise your clients to apply for disability benefits as soon as they become disabled; the process could take several months.

Due to the complexity of the program, to maximize Social Security disability benefits, it is important to help your clients collect all the supporting documents, including medical records, as well as make them aware of their rights in case of denial and appeal requirements.

Key takeaways

- To qualify for Social Security retirement benefits, individuals need 10 years of work history (40 credits), and must be at least 62 years old. Work for at least 35 years to earn enough credit.

- Contributions to Social Security are not tax-exempt or tax-deductible on annual tax returns.

- Full Retirement Age (FRA) varies based on birth year and provides 100% of benefits. For people born on or after 1960, FRA is 67 years.

- Benefits can be delayed until age 70, resulting in higher monthly payments. Claiming it early might result in a potential loss of benefits. Find the right balance.

- Spouses may be eligible for benefits based on their partner’s earnings, maximizing the combined benefit amount. Even dependents may be eligible.

- Remember, you can still earn while claiming the benefits.

- Use tax planning strategies to reduce your other business income to minimize taxes on Social Security income.

====

Bhairavi Parikh, CPA, is a fractional CFO and consulting controller for Analytix Solutions. With more than 15 years of experience in public and private accounting, Bhairavi is well versed in managerial accounting and CFO services for small- to mid-size organizations. After earning her CPA designation in 2004, she spent four years leading a team that was responsible for the internal audit, and internal and external financial reporting for a company with annual revenues in excess of $3 billion.