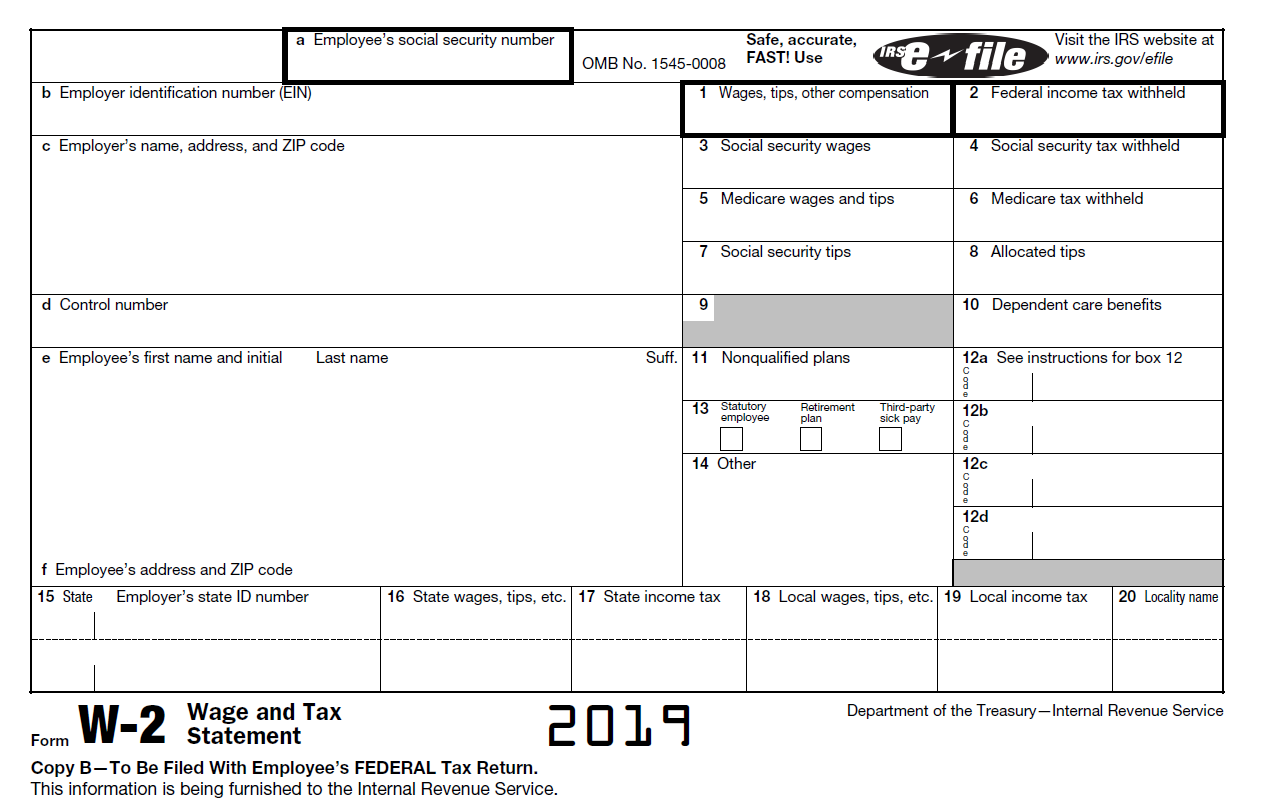

Employers Must File W2 Forms by January 31

A 2015 law made it a permanent requirement that employers file copies of their Form W-2, Wage and Tax Statements, and Form W-3, Transmittal of Wage and Tax Statements, with the Social Security Administration by January 31.

Jan. 19, 2022

Employers are being reminded by the IRS of the January deadline to file Forms W-2 and other wage statements. Filing these documents timely helps employers avoid penalties and helps the IRS in fraud prevention.

A 2015 law made it a permanent requirement that employers file copies of their Form W-2, Wage and Tax Statements, and Form W-3, Transmittal of Wage and Tax Statements, with the Social Security Administration by January 31.

Forms W-2 are normally due to workers by January 31. Forms 1099-MISC, Miscellaneous Information and Forms 1099-NEC, Nonemployee Compensation, are also due to taxpayers by January 31. Various other due dates related to Form 1099-MISC and Form 1099-NEC, including dates due to the IRS, can be found on the form’s instructions at IRS.gov.

Fraud detection

The normal January filing date for wage statements means that the IRS can more easily detect refund fraud by verifying income that individuals report on their tax returns. Employers can help support that process and avoid penalties by filing the forms on time and without errors.

The IRS and SSA encourage all employers to e-file. It is the quickest, most accurate and convenient way to file these forms. For more information about e-filing Forms W-2 and a link to the SSA’s Business Services Online website, visit the SSA’s Employer W-2 Filing Instructions & Information website at SSA.gov/employer.

Use same employer identification number on all forms

Employers should ensure the employer identification number (EIN) on their wage and tax statements (Forms W-2, W-3, etc.) and their payroll tax returns (Forms 941, 943, 944, etc.) match the EIN the IRS assigned to their business. They should not use their social security number (SSN) or Individual Taxpayer Identification number (ITIN) on forms that ask for an EIN.

If an employer used an EIN (including a prior owner’s EIN) on their payroll tax returns that’s different from the EIN reported on their W-3, they should review General Instructions for Forms W-2 and W-3 (.pdf), Box h—Other EIN used this year.

Filing these forms with inconsistent EINs or using another business’s EIN may result in penalties and delays in processing an employer’s returns. Even if an employer uses a third-party payer (such as a Certified Professional Employer Organization, Professional Employer Organization, or other third party) or a different entity within their business to file these documents, the name and EIN on all statements and forms filed must be consistent and exactly match the EIN the IRS assigned to their business. For more information on third-party arrangements, see Publication 15, Employer’s Tax Guide.

Extensions

Employers may request a 30-day extension to file Forms W-2 by submitting a complete application on Form 8809, Application for Extension of Time to File Information Returns by January 31. However, one of the criteria in Section 7 of Form 8809 must be met for the extension to be granted.

Filing Form 8809 does not extend the due date for furnishing wage statements to employees. A separate extension of time to furnish Forms W-2 to employees must be filed by January 31. See Extension of time to furnish Forms W-2 to employees for more information.

Additional information can be found on the instructions for Forms W-2 & W-3 and the Information Return Penalties page at IRS.gov.