This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

And when you make a sale, you need to record the transaction in your accountingbooks. Ten out of 10 businesses sell products or services. How comfortable are you with making a journal entry for sales? How you record the transaction depends on whether your customer pays with cash or uses credit. Read on to […] Read More

Mistakes happen, especially when it comes to recording transactions in your books. One type of accounting mistake thats easy to make is a transposition error. Read on to learn what is a transposition error and how it can affect your accountingbooks. What is a transposition error?

As a small business owner, setting up your accountingbooks and maintaining accurate records is essential. To make that happen, you need to be familiar with accounts payable and accounts receivable. What is the difference between […] READ MORE.

Accounting operates within its own language, a system of terms and conventions that serve as the backbone of financial communication and analysis. Cash vs. Accrual Accounting Cash accounting records transactions only when cash changes hands, providing a real-time view of cash flow.

If you’re running your own business, in Los Angeles, or Orange County, regardless of how large or small your company is, you simply must ensure that you have your books and accounts in order. Here are several tips on managing your accounting. Hire a professional accountant to do it for you. Keep your records organized.

But, how do you record these tax collections and payments in your accountingbooks? Sales tax accounting. You should understand accounting for sales tax to maintain organized and accurate […] READ MORE. When you sell goods to customers, you likely collect and remit sales tax to the government.

Accounting errors are inevitable, especially if you’re rushing to add information into your small business accountingbooks. To detect accounting errors sooner rather than later, learn how to find accounting errors.

Your accountingbooks should reflect how much money you have at your business. If you use double-entry accounting, you also record the amount of money customers owe you. When it comes to your small business, you don’t want to be in the dark. But, what happens if they don’t pay?

Taking steps to clean up accounting records can be a big undertaking for small business owners. You may diligently record your accounting transactions or have hired someone to take care of accounting for you. When and Why You Need to Clean Up Your Books. There are many reasons to have clean accountingbooks each month.

Accounting software is the primary operational tool for bookkeepers and accountants. With a large selection of products available on the market, it’s possible to pick the one that best addresses the unique needs of your accounting firm and your clients. . How to Choose the Right Accounting Software for Your Business?

Accounting is not dependent on the size of the company. Larger companies usually have a team of qualified accountants and bookkeepers who help them achieve accuracy and maintain proper accounting. For mid-sized businesses, however, hiring high-paying accounting staff is not feasible.

Learn how to record the types of revenue in different accounts. That way, you can keep your accountingbooks updated, organized, and legal. To keep business operations running smoothly, you need incoming money. When you make a sale or earn money from another activity, you need to record it. What is revenue?

There are many different accounts you can use to record equity in your business accountingbooks. Before you can begin tracking equity, you must learn about the different types of equity that can apply to your company.

Reconciliation helps you to detect common accounting errors. Referring to your bank statements or accountbooks separately cannot help you to summarize your transactions and balance. Even if you forget to enter any transactions to your accountbook, bank reconciliation statements might help you figure out the correct balance.

Understand the difference between tangible vs. intangible assets to keep your accountingbooks and financial statements accurate. All businesses have assets. Assets can be broken down into two categories: tangible and intangible. Tangible vs. intangible assets Both tangible and intangible assets add value to your business.

Knowing how much inventory you have is crucial for managing accurate small business accountingbooks, ordering new stock, and making pricing decisions. Unless you own a service-based business, you likely have inventory. So, what is inventory? Your small business’s inventory […] READ MORE.

Learn about deferred revenue and how to record it in your accountingbooks. Do customers pay you for your goods or services before you actually deliver them? If so, you need to know about deferred revenue. What is deferred revenue?

When you run a small business, one error in your accountingbooks can result in inaccurate financial statements, poor cash flow management, and even an IRS audit. To make sure your records are accurate, familiarize yourself with account reconciliation. What is account reconciliation?

When you manage your accountingbooks by hand, you are responsible for a lot of nitty-gritty details. One of your responsibilities is creating closing entries at the end of each accounting period. What are closing entries?

Improve cross-department data sharing and visibility Today there’s a greater need for real-time visibility between departments that handle tax and GAAP accountingbooks. ABOUT THE AUTHOR: Evan Croen is senior vice president of product for Bloomberg Tax & Accounting.

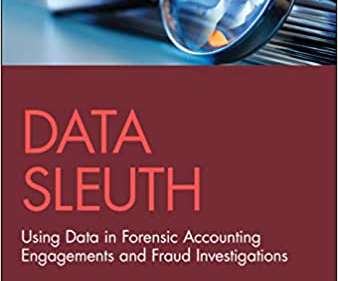

It’s time pre-order the most valuable fraud investigation and forensic accountingbook you will ever read. I had the privilege of previewing Leah Wietholter’s book Data Sleuth: Using Data in Forensic Accounting Engagements and Fraud Investigations. She has knocked this one out of the park.

But the most important aspect of any business is accounting. All small business owners need to be familiar with basic accounting and bookkeeping, as it gives them a clear picture of the state of their finances, allows them to make informed business decisions, and lets them react to any adverse changes faster. What is accounting?

Even in the 21st century, it’s still possible to do your bookkeeping with paper spreadsheets or accountbooks. If manual accounting works for you, nobody can force you to change. Accounting standards are the same whether you use ledgers or laptops. Automated accounting programs save more time and offer more benefits.

Finance and accounting are the foundation of every business, whether it’s a small venture or a large corporation. In this article, we’ll review finance and accounting outsourcing (FAO), in particular its benefits for small and medium businesses. To automate your finance and accounting, sign up for a free trial or book a demo.

As a small business owner, you might not be an accounting wizard, but your math needs to add up. To discover and get to the root of errors in your double-entry accountingbooks, use a trial balance. If you use accrual accounting to manage your books, your credits […] READ MORE.

As a small business owner, you track the money your company earns in your accountingbooks. As a small business owner, you need to account for your company’s […] READ MORE. Can you identify the types of income you record? For example, ordinary income is a common type of income that your business earns.

Having accurate accountingbooks is essential for making financial decisions, securing financing, and drafting financial statements. But sometimes, you find gaps in your records, either from making mistakes or carrying out transactions from one accounting period to another.

You’re constantly entering sales figures in accounts receivable (AR), invoicing customers, remembering whether they’ve paid, contacting them if they haven’t, and adjusting AR when they settle up. One solution is accounts receivable automation. What are Accounts Receivable? This is known as balancing your accounts/books.

Earlier this year I told an accountant that they shouldn’t spend time and money on a website for their practice. The last time I gave such advice to accountant was back in 2018. The accountant to whom I gave my advice earlier this year, is in a very different place to the accountant I was advising in 2018.

An IRS audit is a review of an organization’s or individual’s accounts and financial information to ensure information is reported correctly according to tax laws and to verify the reported amount of tax is correct. Use accounting software to track income, expenses, and deductions throughout the year.

You must know the fair market value of your assets to maintain accurate small business accountingbooks, obtain outside […] READ MORE. And when you sell those assets or buy new ones, you should know their fair market value.

Unplanned expenses, like inventory shrinkage, can lead to a drop in profits and require you to alter your accountingbooks. When running a business, you likely face setbacks due to unforeseen costs. And […] READ MORE.

However, you could end up collecting debts you write off in your accountingbooks. When you offer credit to customers, you may need to write off unpaid receivables as bad debts. If this happens, record the money as a bad debt recovery. What is bad debt recovery? Bad debt recovery, or bad debt collection, is […] READ MORE.

It’s a perfect solution for e-commerce, SaaS business owners, and accountants who need to record many categorized and customized transactions. . Accounting problems with entering and recording PayPal fees. Accounting solution to PayPal transactions problem. Accounting problems with entering and recording PayPal fees.

Footnotes is a collection of stories from around the accounting profession curated by actual humans and published every Friday at 5pm Eastern. And take our 2024 Predictions for the Accounting Profession survey ! Comments are closed on Friday Footnotes and the Monday Morning Accounting News Brief by default.

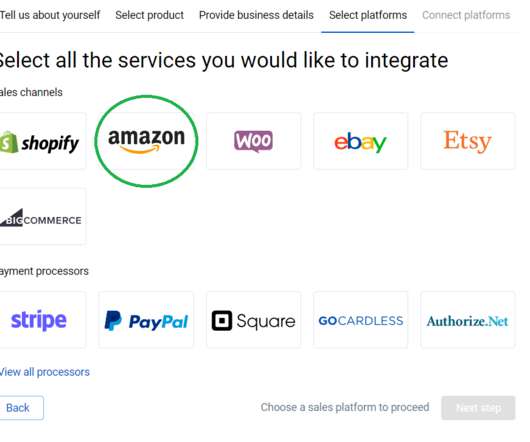

If you’re new to Etsy and want to make sure you’re doing everything right, it’s essential to have a guide on how to set up an Etsy account. You need to provide your personal information, taxpayer address, and state the account to which your deposit will be transferred. Let’s quickly look at each of them. Listing fee.

In business, keeping accountingbooks – records of all the financial operations of your business – is a must. Nowadays the process is made easier by high-quality accounting software which eases the strain of heavy responsibilities. What is the rollback of sync? Why do you need rollback? Rollback of sync with Synder.

Do you have a good command of accounting basics ? The easiest way to keep hold of your accounting is to record transactions with the help of accounting software. With the help of accounting software, you may analyze the following information for your e-commerce business plan: Income statement.

On the other hand, breaking Amazon’s selling policies may lead to serious consequences, such as shutting your account down or Amazon’s withdrawal of your money, so you should always stay honest. The first step towards using FBA is to create an Amazon selling account and log in to Seller Central to set up FBA. Inventory ?

Attestation ledger : A register or accountbook created to provide support/ evidence of individual transactions. Block explorer : A tool people use to view all cryptocurrency transactions online. Block reward : The number of cryptocurrency coins a person gets if they successfully mine a block of the currency.

You can also try making a personal, non-business, social media account, visiting a similar online store to yours, and seeing what targeted ads you get shown. Once you’ve established a community and followers on your Instagram account, it’s time to think about something else. Apply smart automated accounting. But that’s not all.

From advertisements and purchasing additional supplies to covering business taxes, every expense has to be accounted for. You can use an expense report to find out what the business’s biggest expenditure was and how much it cost you during the accounting period. An expense report is a record of expenses incurred by a business.

Still, some products are more suitable as they’re easier to work with and bring more money to your bank account. . It’s easy for everyone to set up an account and start selling online, regardless of their previous experience. This ensures accurate data imports and that there are no duplicates in your accountingbooks.

We organize all of the trending information in your field so you don't have to. Join 237,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content