This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A new proposal that would establish authoritative guidance on the accounting for government grants received by businesses was issued by the FinancialAccountingStandards Board (FASB) on Nov.

The Governmental AccountingStandards Board ( GASB ) has issued guidance that establishes requirements for certain types of capital assets to be disclosed separately for purposes of note disclosures. GASB Statement No. This is designed to allow users to make informed decisions about these and to evaluate accountability.

The Governmental AccountingStandards Board (GASB) issued two exposure drafts on Monday: one on a proposed standard on subsequent events and the other a proposed update to an implementation guide in the form of questions and answers intended to clarify, explain, or elaborate on certain GASB pronouncements.

Contributors: Jack McKee, Manager, Government & Public Sector With staffing challenges and exceedingly more complex GovernmentAccountingStandards Board (GASB) requirements , many government and public sector organizations are finding it difficult to focus on their core mission and deliver results for constituents.

Contributors: Jeffrey Annessa , Artan Ivezaj Government contracts often come with specific requirements, conditions and regulations. Among those regulations are the Cost AccountingStandards (CAS), which are one of the most common challenges faced by emerging government contractors. What Are the 19 Standards?

Statutory reporting is a critical process for multinational corporations, involving the preparation and submission of financialstatements to comply with legal obligations across various jurisdictions. Key components of statutory reports include financialstatements and ESG disclosures, enhancing stakeholder trust and governance.

Several Governmental AccountingStandards Board (GASB) proposals regarding the accounting and financial reporting for infrastructure assets are on the table for stakeholders to review and provide feedback. 10 on the infrastructure assets project, which the standard-setting board said is in its “relatively early stage.”

The Governmental AccountingStandards Board (GASB) issued Statement No. 103: Financial Reporting Model Improvements to provide updated guidance on several areas of the financial reporting model. It is the most significant update to the financial reporting model since GASB Statement No.

The Governmental AccountingStandards Board has issued new guidance that requires state and local governments to disclose information about certain risks. GASB Statement No. This would allow users to make informed decisions about these and to evaluate accountability.

The Board of Trustees of the FinancialAccounting Foundation (FAF) has announced the appointment of Robert W. Scott to a five-year term on the Governmental AccountingStandards Board (GASB). Before entering the public sector, he was employed as an audit manager with the accounting firm of Deloitte & Touche.

Investors, accounting firms, and other stakeholders have until Oct. 21 to provide comments on a new proposed AccountingStandards Update (ASU) issued by the FinancialAccountingStandards Board (FASB) on Tuesday that aims to clarify rules on derivative accounting.

This approach complies with ASC 606 (Revenue from Contracts with Customers), which governs revenue recognition standards in the U.S. Bookkeepers must carefully document and classify these costs to ensure compliance with accountingstandards. This data feeds into financialstatements and cap table management.

Financialsstatements and performance are no different. If incorrect or inaccurate data is used or missing, the financial performance and indicators used to determine success, value, creditworthiness, and financial viability are also not correct. Most of us are familiar with the saying “garbage in, garbage out”.

The Governmental AccountingStandards Board (GASB) issued Statement No. 101 to provide updated guidance on the recognition and measurement of compensated absences for government entities. Objective of GASB Statement No. 101 The primary objective of GASB Statement No.

The Governmental AccountingStandards Board (GASB) has issued Statement No. 102, Certain Risk Disclosures , to provide users of governmentfinancialstatements with essential information about risks related to a government’s vulnerabilities due to certain concentrations or constraints.

The Governmental AccountingStandards Board (GASB) has created a single approach to accounting for and reporting of leases with the issuance of GASB Statement No. 87, Leases (Statement 87). State and local governments should expect Statement 87 to have a significant impact on their financialstatements.

The Governmental AccountingStandards Board (GASB) recently issued Statement No. 102, which adds new disclosure requirements for governments. Numerous risks loom over state and local governments, which could impair their service delivery or hinder their capacity to fulfill obligations in a timely manner.

The Governmental AccountingStandards Board (GASB) recently issued Statement No. 101, Compensated Absences, to update the recognition, measurement and disclosure requirements for compensated absences in state and local governments.

Contributors: DeWanna Coleman Governmental AccountingStandards Board (“GASB”) Statement No. 100, Accounting Changes and Error Corrections—an amendment of GASB Statement No. One government might report an accounting change, while another government might report a similar change as an error correction.

Therefore, when serving business clients, it is important that accounting professionals have the right framework to ensure that proper financial reporting procedures are in place to help with accounting assumptions. What are the main accounting assumptions? Let’s take a closer look at each one. dollars, euros, etc.)

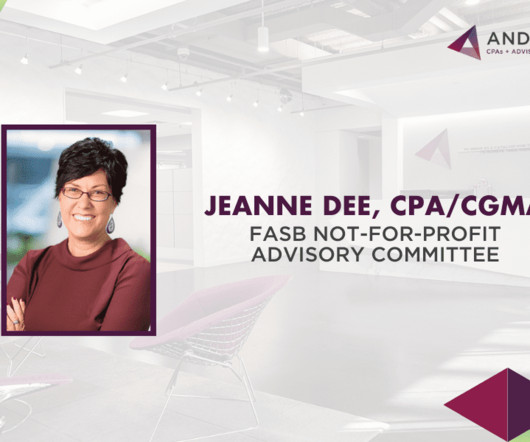

Jeanne Dee, CPA/CGMA, audit and assurance partner at Anders CPAs + Advisors (Anders), has been appointed to the FinancialAccountingStandards Board (FASB) Not-for-Profit Advisory Committee (NAC) effective January 1, 2024. As one of the six new NAC members, Jeanne will serve a four-year term ending on December 31, 2027.

The Governmental AccountingStandards Board (GASB) has issued guidance designed to improve key components of the financial reporting model—the blueprint for governmental financial reports. GASB Statement No.

If the last 20 years of the economy’s highs and lows, downturns and headlines taught us anything about business, it’s that complete and transparent accounting is in everyone’s best interest. One independent organization working to keep companies’ books clear and honest is the FinancialAccountantStandards Board.

After a period of relative inactivity, standard setters have issued four new standards. The FinancialAccountingStandards Board (FASB) has issued AccountingStandard Update (ASU) 2023-03 through ASU 2023-06.

Generally Accepted Accounting Principles (GAAP) are a set of accounting principles, standards, and procedures that define accepted accounting practice at a particular time. Its purpose is to ensure that financialstatements provide an accurate and transparent view of the company’s financial condition and operations.

Over the last year, governmental financialstatement preparers’ attention has shifted from Leases to SBITAs, leaving some to wonder about Public-Private Partnerships (P3s). In its broadest sense, a vendor/customer relationship with a government can be considered a P3. A lease might also be considered a P3.

Contributor: Jack McKee, Manager | Government & Public Sector Governmental AccountingStandards Board (GASB) Statement 96 provides guidance and addresses how the costs and investments for subscription-based information technology arrangements (SBITAs) are accounted for and disclosed by governmental entities.

The Governmental AccountingStandards Board issued an exposure draft on how to account for transactions that occur after the date of the financialstatements.

Accounting’s Big Lie — and How to Fix It [ Project on Government Oversight ] A colossal conflict of interest compromises the auditing of public companies and the financial security of everyone who depends on them. The Project On Government Oversight is planning a conference on what to do about it.

More than 20 years after issuing Statement No. 103, Financial Reporting Model Improvements (GASB 103). Governments should disclose the program, function, or identifiable activity to which an unusual or infrequent item is related and whether it is within the control of management.

For many architecture and engineering (A&E) firms, overhead rate audits are a critical aspect of financial management since they can be a great way for firms to recoup incurred costs necessary to run their business from the government. The firm should ensure that its financialstatements are accurate and up to date.

Ensuring Financial Stability and Growth When Peterson came on board over a year ago, she was tasked with ensuring secure finances and stable growth. Previously, their accounting systems were completely outsourced, taking 60 days (sometimes more) to see a financialstatement.

In Part 1 of our series on Contractor Business Systems, we explore the requirements for a government-approved adequate accounting system as outlined in DFARS 252.242-7006 and required by Federal Acquisition Regulation (FAR) 16.301-3 in the award of a cost-reimbursable type contract.

More than 90% of companies in 90 countries are prioritizing Environmental, Social and Governance (ESG) goals. While it is exciting that organizations are stepping up to pursue responsible practices en masse , the reality is that the onus to comply with related reporting requirements is on accounting and finance professionals.

is in the midst of a long-awaited overhaul of the audit and accounting industry, which will bring with it a new regulator to replace the FRC called the Audit, Reporting and Governance Authority. The new standard becomes effective for audits of financialstatements for periods ending on or after Dec.

In this article, you’ll find the essential information to 38 FAQs about business financialstatements and links to further reading. FinancialStatement FAQs. What is a business financialstatement? The business financialstatement defined. Who uses business financialstatements?

SEC Chief Accountant Lauds FASB for Engaging Investors, Stakeholders on Potential New Standards [ JD Supra ] Paul Munter, acting chief accountant for the SEC’s Office of the Chief Accountant, on Feb.

Business life cycle accounting and reporting challenges For private companies, these challenges can mean fewer staffers who understand accountingstandards, internal systems that are either incomplete or not implemented properly, and potentially insufficient audit preparation when the company goes public.

The GovernmentAccountingStandards Board (GASB) recently issued Statement Number 102, Certain Risk Disclosures (“GASB 102”). GASB 102 requires state and local governments to disclose material concentrations and constraints in the notes of the financialstatements.

At the same time, these entities have an increased need for accounting transparency – and not just because it’s the right thing to do, but also because citizens are demanding it. Without a standardaccounting method, such committed future liabilities and their related intangible assets are not included on financialstatements.

The FinancialAccountingStandards Board (FASB) issued nine AccountingStandard Updates (ASUs), and the GovernmentAccountingStandards Board (GASB) issued only one new GASB Statement in 2023. For summaries of standards issued in the first three quarters, view our previous rundowns here.

The spotlight on environmental, social, and governance (ESG) continues to intensify as businesses are increasingly being called upon to disclose more about their ESG performance and strategies. Risks and opportunities related to ESG matters may have an unfavorable, favorable, or neutral effect on financialstatements.

We organize all of the trending information in your field so you don't have to. Join 237,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content