This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Artificial intelligence, hereafter simply referred to as AI, has evolved momentously over the last decade. But just in the last 6 months, these leaps have been gargantuan. As the discipline relies on data processing, it’s not surprising accounting professionals have been particularly vocal about the advancement of AI (and machine learning) for many years.

Artificial intelligence has been the focus of significant discussion within many professions, among them accounting, tax and legal. How are these professionals facing this new technology with regards to risk and benefit? What are the perils? Thomson Reuters, a global content and technology company, has released new research on generative AI that gauged the sentiment of professionals in legal, tax, and accounting firms in the United States, United Kingdom, and Canada.

Running an eCommerce business comes with challenges, and accounting is a critical aspect that often poses difficulties. Accurate financial records, managing cash flow, ensuring compliance with financial reporting standards, and conducting financial analysis are all essential to running a successful eCommerce venture. However, these tasks can be complex and time-consuming, leading to potential errors and setbacks.

Busy season accounting can in many ways seem unavoidable, but it can be manageable with the right approach. In this post, I’ll lay out 10 simple tips your firm can implement to keep yourself sane and to avoid you from working long hours during the busiest time of the year. Table of Contents Why Does Busy Season Accounting Happen? 10 Tips to Master the Busy Season 1.

In the climb from contributor to leader, the rules quietly change. But if you’re aiming for the summit, the air gets thinner, and what got you here won’t be enough to get you to the top. 🗻 What made you successful early in your finance career—technical accuracy, sharp analysis, flawless execution—won’t be what carries you to the next level. The higher you go, the more your effectiveness depends on how you connect, adapt, and communicate.

Almost five years ago, the Supreme Court’s Wayfair decision was heralded as a revenue gateway for almost all states to require remote sellers to collect and remit sales tax. Thresholds were established, filing forms and deadlines fixed and one by one states waited for the money to roll in (with Florida and Missouri among the latest of the 45, with Alaska perhaps soon to join them).

In adversarial situations — such as divorces, contract breaches and shareholder disputes — you might need to hire an outside business valuator to evaluate complex financial matters. To get the most from these professionals, it’s important to understand the two key roles they can play in conflict resolution. Keeping these roles separate helps prevent valuators from being seen as “hired guns” by judges, juries, arbitrators and mediators.

The IRS miscalculated 2021 child tax credit payments for thousands of eligible taxpayers as of May 5, 2022, according to a new report from the Treasury Inspector General for Tax Administration. The American Rescue Plan Act of 2021, which was approved by Congress and enacted on March 11, 2021, expanded the child tax credit and authorized monthly payments, with differing amounts, to eligible individuals and families based on their adjusted gross incomes and, if they have kids, their children’s age

The IRS miscalculated 2021 child tax credit payments for thousands of eligible taxpayers as of May 5, 2022, according to a new report from the Treasury Inspector General for Tax Administration. The American Rescue Plan Act of 2021, which was approved by Congress and enacted on March 11, 2021, expanded the child tax credit and authorized monthly payments, with differing amounts, to eligible individuals and families based on their adjusted gross incomes and, if they have kids, their children’s age

A new study has revealed that the UK accounting services sector has experienced consistent growth across the country, with increased demand for their services resulting in a 62% increase in new businesses in the sector since 2017. Tyl by NatWest , the payments partner supporting UK SMEs and micro businesses, has commissioned the Evolving Enterprise Index report , revealing the fastest growing and fastest emerging sectors in the UK.

By Emily Fish, director of product accounting at LeaseQuery Within the lease accounting standards, there are exceptions to help entities determine which leases are in scope and which are not. First and foremost, the lease accounting standards apply to all entities—there isn’t an exception for an entity or industry as a whole. Instead, exceptions are applied on a lease-by-lease basis depending on certain policy elections: ASC 842, IFRS 16, and GASB 87 all have exceptions for short-term and immate

In the WaPo opinion pages yesterday one Duncan Mavin, who got his start in the 90s, says the best way to solve the audit industry’s many conflicts is to kill it altogether. He starts the piece summoning the ghost of Enron, as all writers do when discussing what happens when audit goes wrong. Bringing things back to this decade, he then talks about what’s going on at PwC Australia even though auditors weren’t the ones using confidential government data to bill clients for tax av

TaxConnex ® is excited to announce the launch of a new client portal, Client Connexion. Client Connexion will provide a streamlined client experience and enhanced data security through an intuitive user interface and encrypted portal. Clients will be given individual logins to provide their data, review their cash requests, pull reports, and tax returns, and view historical data, thus removing some of the manual processes clients and practitioners navigated through previously.

The most overlooked, yet most critical, element of transformation is preparing people for change. Automation and AI aren't just technical upgrades, they’re cultural shifts which can challenge identities. That’s why change management isn’t a side project—it’s the foundation. In finance, where precision and process rule, navigating change can feel especially disruptive.

Financial statements are central to understanding any business. A public company’s balance sheet, income statement and cash flow statement enable investors, lenders, the media and other stakeholders to value the company, forecast short- and long-term performance, and determine potential credit risk, among other purposes. To ensure analysis of a company is accurate and insightful, financial statements must be reliable.

I have to start by stating that this “Final Notice notice of intent to levy and notice of your rights to a hearing, please respond immediately” is one of the most important and urgent IRS notice a taxpayer may receive, and although it is so important as it would lead to levying your bank accounts, paychecks etc., many taxpayers unintentionally ignore it.

Although personal travel is taking off this summer, business travel is having a more challenging time gaining altitude. Some industry analysts say that it could be well into 2025 before demand returns to pre-pandemic levels. Continued economic uncertainty has organizations carefully balancing budgets and benefits when it comes to corporate travel. But the cost of travel’s carbon footprint is an increasingly important factor in assessing corporate travel cost benefit.

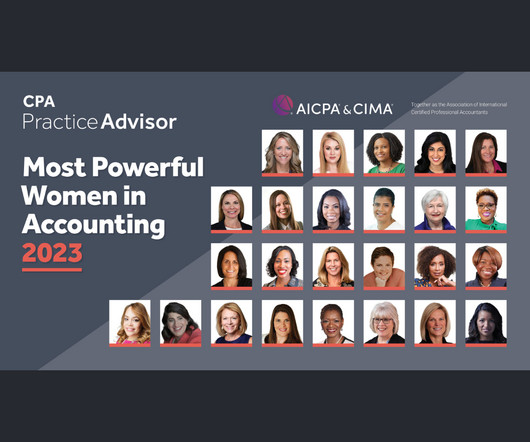

The American Institute of Certified Public Accountants and CPA Practice Advisor have announced the recipients of the 12th annual ‘Most Powerful Women in Accounting’ awards, which recognize leaders for their significant contributions to the profession. The 2023 awards were presented at a ceremony at Dolby Live Stage at the Park MGM Casino during the AICPA ENGAGE conference in Las Vegas on June 6, 2023.

Finance used to be the function that counted, now it's the one that’s counted on. 📊 For accounting firms, controllers, and finance leaders, expectations are rising faster than headcount. Businesses want agile forecasts, granular analysis, seamless reporting, and smart automation—often without added resources while demanding uncompromised accuracy and compliance.

Stock photo of KPMG office in London. Look, the logo is the same ok. Rumors have been buzzing for a few weeks now that KPMG would be making some cuts, the most notable of these buzzes an extra buzzy post on Reddit suggesting an incoming RIF. This morning (Monday), all-hands calls started appearing in people’s calendars and, well, you know what happens after that.

What a major issue for your remote business these days. Constantly changing regulations. Tens of thousands of tax jurisdictions coast to coast, from the biggest states to the tiniest municipalities and everywhere in between. All wanting you to calculate, collect and remit the precise amount of sales tax if you have nexus there. Can all those tax authorities really all keep up with your obligations?

The IRS recently released guidance providing the 2024 inflation-adjusted amounts for Health Savings Accounts (HSAs). HSA fundamentals An HSA is a trust created or organized exclusively for the purpose of paying the “qualified medical expenses” of an “account beneficiary.” An HSA can only be established for the benefit of an “eligible individual” who is covered under a “high-deductible health plan.

Tax problems can be a nightmare for individuals and businesses. It can cause stress, anxiety, and even serious seizure issues if not handled correctly. Tax audits, unpaid back taxes, and unfiled tax returns are just some of the most common tax-related issues that can arise. While dealing with these problems on your own can be overwhelming, hiring a professional tax firm can provide you with a peace of mind and efficient resolution.

Great leadership development is the key to sustainable business growth. Are you ready to design an effective program? HR can use Paycor’s framework to: Set achievable goals. Align employee and company needs. Support different learning styles. Empower the next generation of leaders. Invest in your company’s future with a strong leadership development program.

Startups can face serious penalties for failing to comply with state sales tax laws. If you’ve fallen behind, help is available. The post Sales Tax Compliance: Steps for Startups appeared first on Burkland.

When it comes to financial statements, two key documents play a vital role in providing insights into a company's financial health: the income statement and the balance sheet. While both are important in understanding a company's financial position, they serve different purposes and provide distinct information. In this blog post, we will explore the differences between these two essential financial statements.

Perhaps you’ve already seen this in 24 hours since it was released but let’s talk about it anyway because L-O-f **g-L. UK office furniture company Furniture at Work has published a hilarious anti-WFH piece called “From Claw Hands to Hunchbacks: How Working From Home Could Affect Our Bodies.” The article warns that if you continue to work from home you will end up looking like an enemy from Silent Hill by the time you are 70.

Staying on top of your sales tax obligations is crucial to maintaining compliance and avoiding costly penalties. However, navigating the complex world of sales tax filing is a lot for a business to manage without the right expertise. Fortunately, there are options outside of managing sales tax on your own, but it leaves you with a choice - sales tax software or service provider?

Documents are the backbone of enterprise operations, but they are also a common source of inefficiency. From buried insights to manual handoffs, document-based workflows can quietly stall decision-making and drain resources. For large, complex organizations, legacy systems and siloed processes create friction that AI is uniquely positioned to resolve.

If you’re claiming deductions for business meals or auto expenses, expect the IRS to closely review them. In some cases, taxpayers have incomplete documentation or try to create records months (or years) later. In doing so, they fail to meet the strict substantiation requirements set forth under tax law. Tax auditors are adept at rooting out inconsistencies, omissions and errors in taxpayers’ records, as illustrated by one recent U.S.

Tax matters can be complex and daunting, and navigating the ever-changing tax landscape can be a challenge. In such a scenario, having a qualified tax professional on your side is invaluable. The Enrolled Agent (EA) – a tax specialist authorized by the U.S. Department of Treasury to represent taxpayers before the Internal Revenue Service (IRS).

In the face of global economic turbulence causing widespread disruptions to supply chains, companies are diligently scrutinizing market dynamics to gain insights into consumer behavior and improve demand prediction. Amidst these uncertain times, in-depth demand planning analytics emerges as a crucial strategy for controlling operational expenditures, guaranteeing pleasing customer experiences, and securing long-term profitability.

Startups are quickly adapting to a new normal of constrained VC support and lower valuations. As part of this process, however, founders should also take care to adapt, or at Read More The post The Right Runway: Why Breakeven Will Be Among 2024’s Top Startup Metrics appeared first on Burkland.

Speaker: Claire Grosjean, Global Finance & Operations Executive

Finance teams are drowning in data—but is it actually helping them spend smarter? Without the right approach, excess spending, inefficiencies, and missed opportunities continue to drain profitability. While analytics offers powerful insights, financial intelligence requires more than just numbers—it takes the right blend of automation, strategy, and human expertise.

One of the best things that you can do for your business is to understand financial statements. One of the biggest issues that come with reading financial statements is understanding the differences between Retained Earnings vs Owner’s Equity. The first step is defining the two. Retained Earnings is the company’s net income or loss over the period of the company.

It’s been five years since the U.S. Supreme Court’s Wayfair decision gave tax jurisdictions the power to require out-of-state companies collect and remit sales tax. Those governments jumped on the chance of such revenue and continue to do so. Some facets related to economic nexus are changing in certain states – sometimes for the better for remote sellers, sometimes for the worse.

In recent years, many workers have become engaged in the “gig” economy. You may think of gig workers as those who deliver take-out restaurant meals, walk dogs and drive for ride-hailing services. But so-called gig work seems to be expanding. Today, some nurses have become gig workers and writers in Hollywood who recently went on strike have expressed concerns that screenwriting is becoming part of the gig economy.

Welcome to our comprehensive FAQ guide on the IRS Fresh Start Program ! Dealing with tax issues can be overwhelming, but the Fresh Start Program is designed to provide taxpayers with a second chance. In this article, we’ll answer your most pressing questions about this initiative, explaining its purpose, eligibility requirements, benefits, and how to apply.

Distributed finance teams are rewriting how the back-office runs, and attackers are taking notes. Disconnected workflows, process blind spots, and rising cyber threats are more than just growing pains—they’re liabilities. The challenge isn’t just going remote. It’s building resilient systems that protect accuracy, control, and speed across every transaction and touchpoint.

We organize all of the trending information in your field so you don't have to. Join 237,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content