This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Looking for ways to reduce workload while increasing your firm’s capacity? In this episode, I’ll discuss 2 steps you can take to strategically grow your business while reducing work hours and getting the most out of your capacity. Listen Below. 0:33 – The question I got from social media is relevant to a lot of firm owners: How can busy firm owners find time to work on improving their business and reaching their goals while running the firm?

A business requires accurate, clean books that are updated at least monthly. You have two options to achieve this goal: hire a professional or have a year-end accounting firm handle your bookkeeping. It's OK to ask an outsourced accountant for help with your daily books. Before we get into the reasons, let's first look at how the duties of accountants and bookkeepers differ.

In an era of staffing shortages, accounting firms must increasingly look outside the box to fill gaps in talent. If you find yourself in this position, it may be time to welcome your newest staff member: automation. Historically, accounting firms have dedicated junior staff to handle manual data entry tasks and labor-intensive workflow processes.

The start of a new year always feels fresh. You’re looking ahead and probably getting excited about everything your startup will accomplish in 2023. Don’t forget to look behind you, though. Even as you vision-cast for the year ahead, you need to wrap up the year behind you. Don’t shoot the messenger: it’s time to do your taxes. Yes, you technically have until April 18.

In the climb from contributor to leader, the rules quietly change. But if you’re aiming for the summit, the air gets thinner, and what got you here won’t be enough to get you to the top. 🗻 What made you successful early in your finance career—technical accuracy, sharp analysis, flawless execution—won’t be what carries you to the next level. The higher you go, the more your effectiveness depends on how you connect, adapt, and communicate.

When we talk about why no one wants to be an accountant anymore, a handful of things come up in every thread. Let’s quickly get them down in case an alien who just landed on Earth this morning Googles “accountant shortage,” arrives on this article, and wishes to learn more about the causes. Salaries — starting salaries in particular — that do not compete with other white collar and professional services fields; Poor work-life balance that has only gotten worse as st

If your business is scaling, it’s likely that so is your finance team. But no matter the size, with tracking and paying expenses, making payroll, setting budgets, preparing for the tax season, and more all falling under one department, you’re likely looking for ways to make managing financial processes easier and more transparent. Take expenses, for example.

If your business is scaling, it’s likely that so is your finance team. But no matter the size, with tracking and paying expenses, making payroll, setting budgets, preparing for the tax season, and more all falling under one department, you’re likely looking for ways to make managing financial processes easier and more transparent. Take expenses, for example.

Over the years, my conversations with sole practitioner accountants reveal that many are “happy enough” once their practice is generating sufficient income for them. They have reached the stage where they feel comfortable, some might say, complacent. ‘Happy enough’ is hardly an enthusiastic summation of how things are going as it can imply a reluctant acceptance of the status quo.

If you’re a parent or grandparent with college-bound children, you may want to save to fund future education costs. Here are several approaches to take maximum advantage of the tax-favored ways to save that may be available to you. Savings bonds Series EE U.S. savings bonds offer two tax-saving opportunities when used to finance college expenses: You don’t have to report the interest on the bonds for federal tax purposes until the bonds are cashed in, and Interest on “qualified” Series EE (and

When viewed unemotionally with the company’s best interests in mind, a down round may be the best way to get fresh capital in the door. The post Founders: Is It Time to Consider a Down Round? appeared first on Burkland.

A taxpayer who deducted expenses attributable to the business use of his vehicles took a wrong turn before the Tax Court. Ultimately, he wasn’t able to back up his claims (Eze, TC Memo 2022-83, 8/4/22). Generally, you can deduct costs relating to the business use of your vehicle, subject to certain rules and limits. However, you must meet strict substantiation requirements spelled out by the IRS.

The most overlooked, yet most critical, element of transformation is preparing people for change. Automation and AI aren't just technical upgrades, they’re cultural shifts which can challenge identities. That’s why change management isn’t a side project—it’s the foundation. In finance, where precision and process rule, navigating change can feel especially disruptive.

Think you’re the only one worried about sales tax compliance? According to our third annual Sales Tax Market Survey you’re not. “Our company is highly acquisitive and this results in lack of consistency when it comes to billing, accounting and reporting,” said one survey respondent. “Increasingly, I am finding the people who ‘know’ the products and classified them for tax coding purposes long before I arrived do not understand the importance of the little details that can make a huge difference

If your small business has a retirement plan, and even if it doesn’t, you may see changes and benefits from a new law. The Setting Every Community Up for Retirement Enhancement 2.0 Act (SECURE 2.0) was recently signed into law. Provisions in the law will kick in over several years. SECURE 2.0 is meant to build on the original SECURE Act, which was signed into law in 2019.

Selecting the right inventory planning solution is critical for efficient supply chain management. As the amount of data increases, organizations want to invest in a complete planning solution that can connect to multiple data sources, extract, and optimize data models, and offer accurate demand forecasts that can help manage optimal inventory levels.

After several days of requests by taxpayers, state agencies and the National Taxpayer Advocate , the Internal Revenue Service has provided clarifying the federal tax status involving special payments made by 21 states in 2022. The IRS has determined that in the interest of sound tax administration and other factors, taxpayers in many states will not need to report these payments on their 2022 tax returns.

Finance used to be the function that counted, now it's the one that’s counted on. 📊 For accounting firms, controllers, and finance leaders, expectations are rising faster than headcount. Businesses want agile forecasts, granular analysis, seamless reporting, and smart automation—often without added resources while demanding uncompromised accuracy and compliance.

Reference this handy checklist to understand pay transparency compliance requirements and avoid fines at your startup. The post Avoid Fines: The Pay Transparency Checklist appeared first on Burkland.

Are you worried your business won’t receive what a liquidating creditor owes it? In most cases, liquidating companies come by their financially distressed situations honestly. But there’s always a chance that a debtor has made fraudulent transfers or taken other steps to hide assets from creditors. A solvency expert can help you and your legal counsel determine whether a liquidating business is capable of meeting its interest and repayment obligations.

Candy, flowers, diamonds, romantic dinners out or a movie snuggled on the couch: The year’s biggest day for dates looms again, and here’s an update on sales tax considerations for Valentine’s Day. Expected spending on gifts this year should average $192.80, up almost 10% from last year, according to the National Retail Foundation. Once again, the top shopping destination to purchase Valentine’s Day gifts is online (35%), closely followed by department stores (34%) and discount stores (31%).

By Rachel Blakely-Gray. The new W-4 form for 2023 is now available. Unlike the big W-4 form shakeup of 2020, there aren’t significant changes to the new form. But that doesn’t mean you shouldn’t familiarize yourself with it. You may not file Form W-4 with the IRS, but your payroll depends on it. Employers use Form W-4 to determine how much to withhold from an employee’s gross wages for federal income tax.

Great leadership development is the key to sustainable business growth. Are you ready to design an effective program? HR can use Paycor’s framework to: Set achievable goals. Align employee and company needs. Support different learning styles. Empower the next generation of leaders. Invest in your company’s future with a strong leadership development program.

The new tier will enable accountants to get all their QuickBooks transaction questions resolved from their clients quickly and easily—and the subscription is free.

Historical financial results are only relevant in a valuation to the extent that the business expects to achieve similar results in the coming years. When projecting future economic benefits, it’s important to consider expected changes to a subject company’s internal and external conditions. Challenging the status quo The last three to five years of financial statements are usually on the list of documents experts use to value a business.

It was only a couple days ago that the Journal of Accountancy published an interview with NASBA CEO and President Ken Bishop in which Bishop sternly warns states against even thinking about lowering the CPA licensure requirement to 120 units, something something mobility blah blah. To save you a click, here’s a relevant snip of that JofA article and his comments, published February 10: “Should any state or jurisdiction lower the licensure requirement to 120 hours, their CPAs would no longe

Do you want your team to feel empowered and motivated? It starts with establishing a solid foundation of an employee-first culture. When employees feel valued, respected, and supported by leadership, your firm builds and sustains trust in its talent. This kind of atmosphere leads to increased job satisfaction for every team member in the firm and has far-reaching impacts on productivity, morale and collaboration—all key elements that drive success.

Distributed finance teams are rewriting how the back-office runs, and attackers are taking notes. Disconnected workflows, process blind spots, and rising cyber threats are more than just growing pains—they’re liabilities. The challenge isn’t just going remote. It’s building resilient systems that protect accuracy, control, and speed across every transaction and touchpoint.

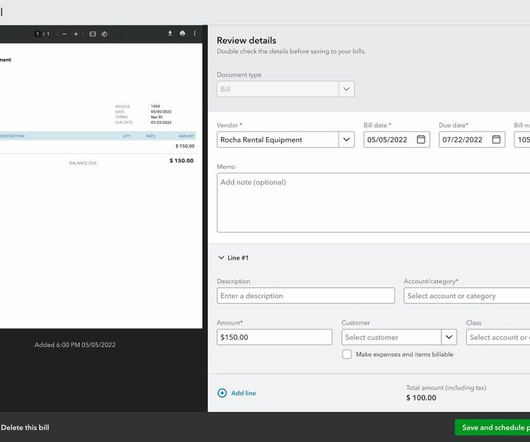

Murph brings you up to date on the vision that is the QuickBooks Business Network. While it's not fully capable yet, it's getting there, and appears to be heading in the right direction.

Technology advancements are continuously reshaping not only the way we work, but fundamentally how we operate across nearly every industry. With new innovations unlocked almost daily — each with a unique promise to transform how we do business — how do busy small businesses and their advisors separate the fad from the fancy? We’ve been doing a lot of thinking about this recently, and it’s a priority for us this year to help demystify some of these trends and shine a light on those which could be

Earlier this month, short seller Hindenburg Research dropped a report called Adani Group: How The World’s 3rd Richest Man Is Pulling The Largest Con In Corporate History (report here ) full of bullet points outlining the findings of Hindenburg’s two-year investigation into the Indian conglomerate. Among the various accusations: shoddy controls, nepotism, questionable shell company relations, and poor transparency (we’re being mild here).

The Department of the Treasury and the Internal Revenue Service have provided new guidance to establish a program to provide solar and wind power to certain low-income areas under the Inflation Reduction Act. Notice 2023-17 (.pdf) establishes the Low-Income Communities Bonus Credit Program and provides initial guidance for potential applicants for allocations of calendar year 2023 capacity limitation.

Documents are the backbone of enterprise operations, but they are also a common source of inefficiency. From buried insights to manual handoffs, document-based workflows can quietly stall decision-making and drain resources. For large, complex organizations, legacy systems and siloed processes create friction that AI is uniquely positioned to resolve.

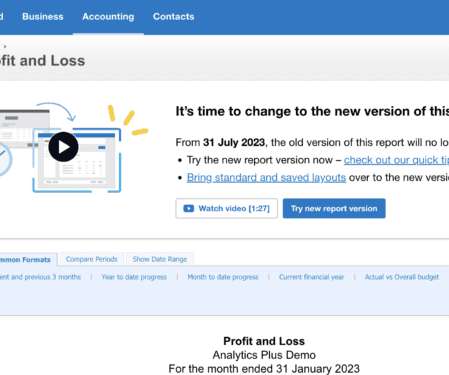

The retirement of old reports is now only a little over five months away. If you’re like many small business owners and advisors, you’re probably starting to seriously think about how this will impact your day-to-day work. We’ve answered some of your most common questions, so you can feel confident about switching to new reports before 31 July 2023.

Are we ready for another survey? OH BOY. Thomson Reuters has written up the 2022 ConvergenceCoaching, LLC® Anytime, Anywhere Work (ATAWW) Survey — you can request survey results here — and we learn that almost all responding firms say they are being flexible about where and when their people put in their time. Of the 216 accounting firms that participated in the 2022 ATAWW Survey, 97% allowed their talent to choose where they work, while 94% offer flexibility in when people are worki

By Christina Luttrell, Chief Executive Officer for GBG Americas ( Acuant and IDology ). Tax season is always stressful. Hurried filers inundate tax preparers working furiously to help their clients file on time while the dreaded tax deadline looms. However, it’s important to pause and reflect on your data privacy standards, digital communication norms, and potential vulnerabilities this tax season.

Speaker: Claire Grosjean, Global Finance & Operations Executive

Finance teams are drowning in data—but is it actually helping them spend smarter? Without the right approach, excess spending, inefficiencies, and missed opportunities continue to drain profitability. While analytics offers powerful insights, financial intelligence requires more than just numbers—it takes the right blend of automation, strategy, and human expertise.

We organize all of the trending information in your field so you don't have to. Join 237,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content